In this article, I want to share some information on the advantages of delaying your Social Security benefits. Industry research has confirmed that most retirees benefit from delaying Social Security payments. There are, of course, reasons why people don’t do this even though it might benefit them to do so. Some simply need the money now rather than later. Some have health issues which cause them to think they might not live to a very old age. And some have a bird-in-the-hand philosophy.

The key to understanding this is something called the full retirement age or “FRA” (also called the normal retirement age). Taking Social Security before the full retirement age decreases your monthly benefit. Taking it after that age increases your monthly benefit due to delayed retirement credits of 8% per year (under current law). So if you can wait until age 70, your monthly benefits will increase by 77% (compared to claiming at age 62). Note that benefits do not increase after age 70.

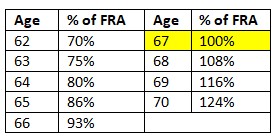

The full retirement age varies slightly depending on when you were born. (The full retirement age is age 65 if you were born in 1937 or earlier. It’s 67 if you were born in 1960 or later.) If you were born in 1960 or later, the following table describes how your benefits increase or decrease depending on when you start taking Social Security.

If you’re able to wait, here are some of the reasons that delaying payments often makes a lot of sense. First, there are the higher monthly payments that I mentioned. Another very important reason to wait is that doing so will increase the chances that you’ll have enough income should you live to a ripe old age. Running out of money is a top concern of retirees and delayed Social Security can really help out here. Another reason to wait is that research has shown that Social Security returns are superior to annuities, bonds and equities in many ways. Finally, delayed Social Security benefits can help protect you against increased inflation and down markets. The very things that your other investments are not immune from.

Outside of these when-to-start considerations, it’s important to coordinate starting dates with your spouse to maximize your combined monthly income. Guidepost Financial Planning can help you sort through your options. Please visit our website or give us a call at 970.419.8212 so that we can discuss your financial goals in a no-charge, no-obligation initial meeting.

This article is for informational purposes only. This website does not provide tax or investment advice, nor is it an offer or solicitation of any kind to buy or sell any investment products. Please consult your tax or investment advisor for specific advice.