As you know, inflation has been generally on the rise. Inflation simply means an increase in what we have to pay for goods and services. We feel it at the gas pump, in the grocery store and when we try to finance a major purchase like a new home. The rate of inflation was at 8.5% in July 2022. The Federal Reserve has been trying to reduce inflation by raising the interest rates for banks to borrow funds from each other. The last two interest rate changes have been a very high 0.75% per increase. This has landed us at a 2.4% interest rate as of July 2022. Some experts believe it could even reach about 4% by the end of the year. This month we’ll take a look at a few of the important things you might consider in this inflationary period of rising interest rates.

Investments

One good thing about inflation is that the rates paid by financial institutions generally rise. They lag the Federal Reserve increases and are lower, but they do go up. The bad news is that even though interest earned goes up, your spending power still goes down. Nonetheless, it makes sense to try and maximize returns.

The most important thing you can do is monitor the rates that are being paid for your money. For example, online banking typically outperforms local brick-and-mortar banks. At the moment, several online banks offer interest in the 1.75-2.15% range with their high-yield money market accounts. Treasury bills are another option. They are currently paying 3.26% for a one-year investment. When inflation is high, a very interesting option is I Bonds from Treasury Direct. They are fully insured government bonds whose rate is tied to inflation. Currently their interest rate is 9.62%. Yep, 9.62%! What’s the catch? Nothing really, except there are a few important things to be aware of. First, you can only invest $10,000 per person per calendar year. So, if you’re a couple, that’s still $20,000. Have a trust? They qualify for $10,000 as well. Second, the rate is adjusted every six months. Third, you can’t cash these in until after a year. So, they’re kind of like CDs in that regard. Fourth, if you cash them in before 5 years, you lose three month’s interest.

Debt

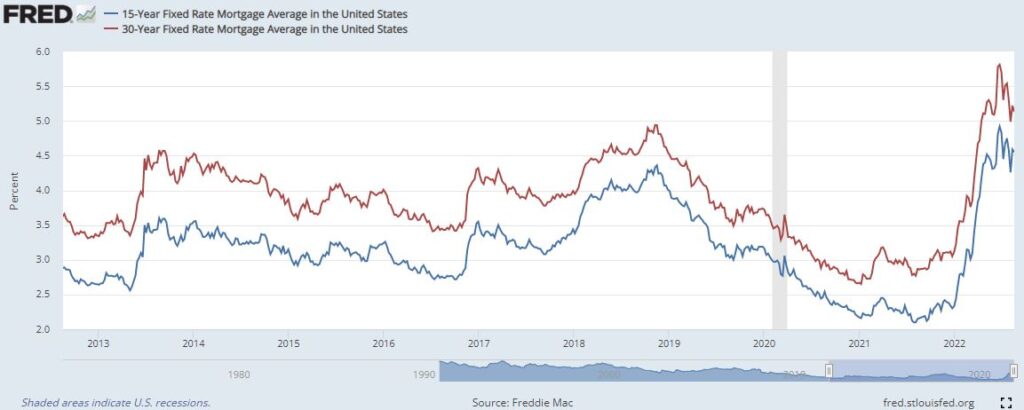

The interest charge on debt is directly related to the Federal Reserve rate. As the Fed raises interest, you’ll pay more for new debt. For existing debt, it depends on whether your rate is fixed or whether it’s variable. So, you may have a fixed-rate mortgage and that cannot change. On the other hand, if you are a first-time buyer or are thinking about refinancing your mortgage, you’ll pay more as inflation rises. As a reminder of mortgage rates, here’s a chart for the last 10 years.

It’s the same story for auto loans and other major purchases. If you carry a lot of credit card debt, the rate is already very high and will probably increase as the Fed raises rates.

The best way for you to deal with rising inflation will depend on your particular situation. If you’d like to discuss this in more depth, or go over any other financial matter, we can discuss things in a no-charge, no-obligation initial meeting. Please visit our website or give us a call at 970.419.8212 to set up an in-person or virtual meeting.

This article is for informational purposes only. This website does not provide tax or investment advice, nor is it an offer or solicitation of any kind to buy or sell any investment products. Please consult your tax or investment advisor for specific advice.